Texas’ Largest Corporate Welfare Program is Rapidly Ballooning

The program will cost taxpayers at least $8.5 billion over its lifetime, according to an Observer analysis.

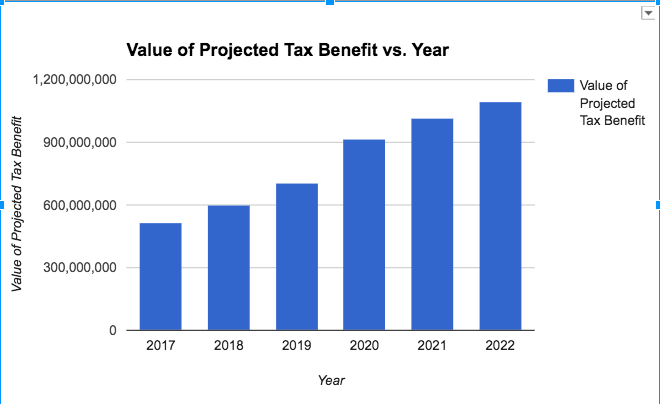

The Texas Economic Development Act, the state’s largest corporate welfare program, has grown rapidly over the last decade and will cost taxpayers at least $8.5 billion in property tax breaks to businesses through its lifetime, according to an Observer analysis of data from the comptroller’s office. That’s money that comes out of the struggling public school finance system. Last year, Chapter 313 bled $326 million from Texas schools, and it’s projected to grow to $1.1 billion per year by 2022.

Commonly called Chapter 313 for its place in the tax code, the program was created by the Legislature in 2001 based in part on a typo in a report that showed Texas losing its competitive edge to other states. Lawmakers believed that Texas needed to offer big breaks on property taxes to lure business to the state. Under Chapter 313, school districts can strike deals with corporations to reduce their property tax obligations by up to 90 percent for 10 years. Because the state picks up the tab and companies often sweeten the pot with supplemental payments, there’s little incentive for school districts not to agree.

There is no limit to how much Chapter 313 could cost the Texas public school system. As the Observer has reported, the comptroller’s office, which oversees the program, almost never rejects a proposal, routinely signing off on tax breaks to companies that couldn’t have located in another state or were already planning to build in Texas.

“The big issue is why is it getting so big so fast,” said Dick Lavine, a senior fiscal analyst at the liberal nonprofit Center for Public Policy Priorities. “The answer is because we’re giving tax breaks to companies that were coming to Texas anyway. There’s a lot of revenue being unnecessarily lost to [these] companies.”

In 2009, Texas schools had struck deals for 90 projects that cost the state about $2 billion. Six years later, the program had grown to 259 projects receiving tax breaks worth about $5.5 billion. As of last May, there were 311 projects on the books that will vacuum $7 billion from the state budget, according to a report submitted by the comptroller’s office to the Legislature. But legislators don’t have the most up-to-date information.

Relying on a new comptroller report published earlier this month, the Observer calculated that the total lifetime cost of the program is at least $8.5 billion, when projects approved in the last half of 2016 are included.

Lauren Willis, a spokesperson for the comptroller’s office, didn’t refute the Observer’s analysis and simply pointed out that the report to the Legislature didn’t include projects finalized after May 15 and growth projections for the program. (A spreadsheet of the Observer’s calculations can be found here and an explanation of our methodology can be found here.)

Skeptics have long criticized Chapter 313 for providing tax breaks to projects that couldn’t be built elsewhere or were coming to Texas anyway. To qualify, companies merely have to assert that the tax break was “a determining factor” in deciding to locate in Texas.

“There’s no competition for these companies,” said Nathan Jensen, a University of Texas at Austin government professor who has been studying the program. “The unlimited amount of incentives that has been offered here is incredible.”

State senator Lois Kolkhorst, who has pushed to reform Chapter 313, told the Observer in an email that she’s “had concerns about the program for years.” Companies are required to create a minimum number of jobs in order to be eligible for the program, but the comptroller doesn’t verify the jobs data reported by the company.

“It’s in some ways similar to an honor system,” she said. “An applicant claims a certain amount of jobs will be created, the property tax break is then given to them and there is very little follow up.”

Kolkhorst, who reviewed the Observer’s analysis, said the comptroller was doing “as well as possible” considering they are required by law to report the fiscal effect on the state to the Legislature, but do not have specific mandates on how up-to-date the information must be.

In some cases, the comptroller appears to have greenlighted projects for applicants that either provided misleading information or openly admitted to not having considered locations in other states.

In December, the Observer reported that Energy Transfer Partners, the Dallas company behind the Dakota Access Pipeline in North Dakota and the Trans Pecos Pipeline in the Big Bend region, had already invested millions of dollars in the projects it was pitching to the comptroller’s office before applying for the tax break.

In one case, Energy Transfer Partners told its investors that it was planning on building a natural gas plant in East Texas around the same time that it was threatening the comptroller’s office with moving the facility elsewhere if it didn’t receive the tax break.

Other companies have been less savvy. Among the earliest Chapter 313 projects was a petrochemical plant operated by Sabina Petrochemicals LLC. In its application, Sabina claimed it “gave serious consideration” to locating in Deer Park before picking the Port Arthur location. Deer Park is on the outskirts of Houston, near Pasadena. The comptroller’s office still approved the $15.9 million tax break.

“The rules have been written in a way that it’s very difficult to be rejected [by the comptroller’s office],” said Jensen.

Willis, the spokesperson for the comptroller’s office, said in an email that the agency “stand[s] by [their] process for all of the projects that have received Ch. 313 agreements” and that the Sabina application was approved under a 2002 law that held the local school district solely responsible for vetting project applications.

A 2016 Texas Senate report also concluded that the comptroller was approving projects that would have been built in Texas anyway. On wind projects, for instance, the authors noted that state-financed transmission lines and an isolated grid make Texas an attractive proposition for developers and would likely have brought wind turbines to Texas without the incentives. And of the 116 manufacturing projects the report’s authors analyzed, 83 were located in districts bordering a major shipping port and were close to a network of refineries and pipeline systems that are likely an advantage for petroleum product processing and manufacturing companies.

“Both the wind projects and the manufacturing projects, which collectively account for 94% of all Chapter 313 agreements, have ample reasons for locating in Texas aside from Chapter 313,” the authors concluded.

“It makes sense to offer incentives to a business that can relocate to a variety of places without regard to any geographic concerns,” Kolkhorst said. “But it makes absolutely no sense to entice a business that is restricted in its location by geographic considerations.”

Kolkhorst has filed a bill that would require the comptroller’s office to verify the jobs data and other details companies provide with information from the Texas Workforce Commission.

You May Also Like

When the AI Cloud Comes for Texas Water

Legislators are (sort of) beginning to grapple with the grim costs that come with the state’s data center boom.

How Teach for America Helped Set Up James Talarico’s Political Rise

The prestigious education group is more than a shiny résumé item. For the Democratic Senate candidate, it was an incubator for his rapid political ascent.

Who Accounts for Freedom?

The nascent school voucher program is, predictably, burdened by Republicans’ insistence on religious discrimination—and likely set to benefit those already outside the public school system.