As Texas’ $10 Billion Corporate Tax Break Program Closes, State Comptroller Wants to Cover Up Costs

With Chapter 313 set to expire, the Texas Comptroller has proposed new rules that critics warn would reduce accountability and transparency, shrouding its long-term costs in secrecy.

Texas Comptroller Glenn Hegar is pursuing new rules that opponents warn would weaken transparency and accountability for the state’s biggest corporate tax break program, Chapter 313, just as it is set to expire at the end of 2022. The comptroller’s proposals, which were published last Friday, would effectively cover the program in a cloak of opacity, obscuring the billions of dollars that the state will still be on the hook for even after the program shuts its doors. Hundreds of these lucrative school property tax deals are still in their early years—or still awaiting approval—and will remain active for decades to come, as far out as 2049.

The hulking property tax abatement program met its unexpected demise this year when state lawmakers chose not to renew it. For years, Chapter 313 has allowed local school districts to grant corporations steep discounts on property tax bills for 10 years in exchange for building large-scale projects. The program was a coup for major manufacturing firms, oil and gas giants, and other large corporations that have saved billions of dollars on school property taxes since the Chapter 313’s inception 20 years ago.

But support for the once-popular program flagged amid concerns about its rapidly ballooning size, at last count, of 600 active projects and an estimated total lifetime cost of roughly $11 billion in foregone tax revenue. Chapter 313 also drew scrutiny over its biggest selling points: that these projects—which technically would only happen because of these deals—create lots of high-paying quality jobs and that the value these facilities bring to school tax rolls over the long-term easily outweigh the cost of a decades worth of tax breaks.

The data and reports that the comptroller is proposing to get rid of or make less accessible have allowed for several exposés uncovering the program’s many flaws. A recent Texas Observer investigation into the Chapter 313 deals that have now come to an end found that companies often drastically overestimated how much value the projects will bring back to the tax rolls. A Houston Chronicle investigation also found that corporations routinely failed to create the required job and wage requirements once they secured the tax incentives.

The Comptroller’s Office, which administers Chapter 313, has decided the best response to these findings is to simply do away with the pesky data collection and value projections and weaken job reporting requirements.

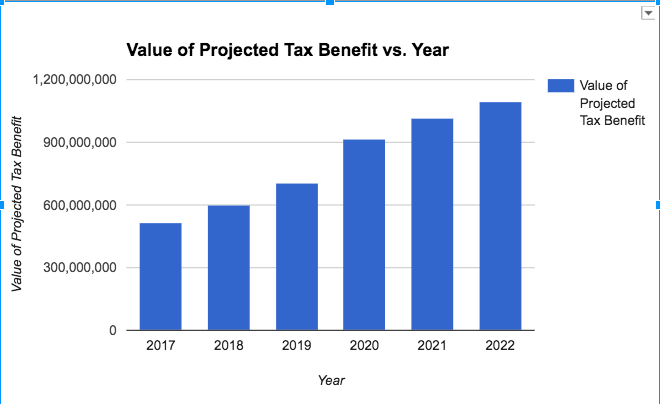

First, the comptroller wants to do away with the biennial reports that require companies to provide actual and estimated figures for a project’s market value, taxable value, and annual gross tax benefits for the entire lifespan of their Chapter 313 agreements—including for a number of years after the tax breaks end. This data provides critical information on the projected long-term costs and benefits of the program. For instance, the comptroller uses that data to forecast the total amount of tax revenue that is foregone because of the program each year. (The annual cost of the tax breaks is currently projected to surpass $1 billion a year in 2023.)

That dataset is a powerful tool for analysis and accountability. That data revealed that companies applying for 313 deals routinely make wildly optimistic projections about how much their projects will generate once they return to tax rolls.

“This would completely hamstring the Legislature, the media, and the public from having any idea of the enormous ongoing costs of Chapter 313 to the state and to public education financing,” says Dick Lavine, senior fiscal analyst for the progressive policy group Every Texan and a fervent critic of the program.

For instance, the Observer found that the 16 manufacturing projects—mostly oil refineries and petrochemical plants —that have reached the end of their tax limitations returned to the rolls at a collective value of $3.5 billion. That was less than half of the $7 billion the projects were worth at their peak and just 20 percent of the $18 billion in total investment.

That same analysis would likely be impossible to do if the comptroller ends its current data collection. The proposed rules would replace the current biennial reporting requirements with a pared-down form that requires companies to report the actual values of their projects for only the two most recent years. It’s unclear how that data would be compiled over the years, nor how the public will be able to review it.

The comptroller also wants to change the annual reports that ostensibly ensure that each project is meeting job and wage requirements. Currently, companies file the reports with the local school district, which then submits it to the comptroller, which in turn posts the report to the agency’s website. This makes reports easy to access for the public. Now, the comptroller wants to relieve school districts of that responsibility, meaning that there would no longer be a central hub for these required job reports. As Lavine explains, the change “would require [hundreds of] individual requests to school districts to get the jobs and wage numbers” for all the individual projects.

Last week, Robert Wood, the agency official who is handling the wind-down of Chapter 313, offered another rationale for the upcoming changes at an online conference for the Texas Taxpayers and Research Association—a key Chapter 313 booster whose members are among the biggest beneficiaries of the tax breaks. Wood said that the agency planned to reduce reporting requirements for companies because the program is coming to an end. “I think the obvious thing is the level of information that we need on an ongoing basis may not be the same as it was when you have an operational program that’s continuing into the future,” Wood said. He also said that the less intensive reporting requirements would free up agency resources “so that we have staff in order to process as many of these applications through 2022 as we can.” During the presentation, Wood counseled companies to start preparing their 313 applications as soon as possible if they want to get approved before the December 2022 deadline.

“My advice,” he said, is to “start early.”

The Comptroller’s Office claims that the proposed changes are about modernization and streamlining. “The proposed changes to the forms will bring the Chapter 313 reporting system into the digital age, making access by the public simpler and reducing the burden on school districts and agreement holders,” the agency states on its website. “The proposed rule replaces the paper-based reporting system with an online system to simplify the reporting process and reduce time and expense required to comply with the administrative rules.” But that explanation is rather confusing. Farther down on the same webpage, the comptroller says that the forms it proposes doing away with are already “electronic-only spreadsheets” and that “hard-copy” forms are not accepted.

In response to questions about the proposals, the Comptroller’s office said the current data reporting requirements are no longer needed with the program set to close and that the long-term estimates were often unreliable. “The [cost data request] form was created years ago primarily for the purpose of allowing the Comptroller to make projections related to potential changes with each legislative session. With the expiration of the program, the future cost estimates are of diminished value, since no future changes to the program will be made,” the statement reads. “Additionally, requiring school districts and companies to provide estimates for local tax rates, company investment, market value, and other information up to 15 years into the future has proven to be challenging due to ever-changing market and economic conditions.”

Regarding the proposal to stop posting annual job report data, the statement said that, “Requiring the reports to be submitted to the comptroller was never contemplated by the legislature and is redundant.”

The public has until December 19 to submit comments to the agency.

The Comptroller’s rationale for curtailing Chapter 313 reporting requirements strikes the program’s critics, such as Lavine, as nonsensical. While the program is coming to a close, the magnitude of its costs is only just beginning to be felt.

“There will be a flood of new applications in the next year as companies rush to take advantage of the expiring tax break,” says Lavine. “Which means future costs will be even greater than previously projected. And under the comptroller’s proposed rules, we will have no idea how large those costs will be.”

Already, roughly 100 new applications have rushed in since the end of the Legislature’s regular session this spring and many more are likely to come in the next several months. In September, Texas Instruments filed four separate Chapter 313 applications with a North Texas school district for a $30 billion factory project. One application proposes an agreement with tax breaks that won’t begin until 2040.

You May Also Like

Texas’ Largest Corporate Welfare Program Is Leaving Companies Flush and School Districts Broke

The state’s Chapter 313 program offers steep discounts on property taxes to attract big industrial projects that are supposed to pay off over the long term. But by the time these projects return to the tax rolls, much of that value has disappeared.

Study: Texas Spent $4.4 Billion Luring Businesses That Were Coming to the State Anyway

About 85 percent of the projects that received tax breaks through the Chapter 313 program didn’t need the incentive, according to a new study.

Texas’ Largest Corporate Welfare Program is Rapidly Ballooning

The program will cost taxpayers at least $8.5 billion over its lifetime, according to an Observer analysis.