How the Payday Loan Industry Works Regulators from the Inside

I think it’s probably safe to say that before he disparaged his customers to the El Paso Times, virtually no one had heard of William White, the chairman of the Texas Finance Commission and a Cash America executive. (Well, the Observer did write about him in 2011.) Getting into the holiday spirit, in late December White suggested to the Times that the reason people take out unregulated, 500-plus percent APR payday loans is to buy a “60-inch TV” and should “pay the consequences” for their terrible decision to use one of his company’s products.

The comments set off a firestorm of criticism, culminating in Sen. Wendy Davis’ call for White to resign—a demand she formalized in a letter to Gov. Perry yesterday. What White has done is give Davis an opening to talk about an issue she’s long been a leader on, and to put opponent Greg Abbott on the spot. The Quorum Report‘s Harvey Kronberg noted that “Abbott’s silence gives the Davis Campaign room to claim that Abbott is just Governor Perry’s ‘pay to play’ redux.”

White’s remarks also point to just how deeply rooted the payday loan industry has become in state government. Davis and others are reaching for that old Texas metaphor, “the fox in the henhouse,” to describe just what’s wrong with the situation. But what, exactly, is the fox doing in the henhouse (other than grinning through a mouthful of feathers)?

White and his company, Cash America, documents show, have been intimately involved in trying to undermine the efforts of Texas’ big cities to regulate payday and auto-title loans at the municipal level. And in his role as finance chair, he was instrumental in passing a resolution against tighter regulation—one that the payday loan industry used to its advantage at the Legislature. While White oversaw the Texas Finance Commission, his colleagues at Cash America worked behind closed doors to draft legislation with regulators.

The biggest challenge the payday loan industry has faced in Texas over the past few years is arguably a rear-guard action by Texas’ big cities. Over the past few years, every big city in the state has passed ordinances regulating consumer loans within their city limits. On Tuesday, El Paso reaffirmed its ordinance. The industry has fiercely opposed the local efforts, launching PR campaigns, a lobbying blitz at the Capitol and suing some of the cities. Absent city rules, payday and auto-title lenders would be free of almost any Texas regulations.

While payday loan interests claim the ordinance is unenforceable, the rules—which include limits on the size of loans, the number of times borrowers can “roll over” the loan and disclosure requirements—have clearly had an impact on the companies’ bottom lines. We know this thanks to Cash America.

In a conference call with analysts in October, CEO Daniel Feehan complained that his Texas payday loan business was “very quickly and negatively affected by the city ordinances.” Feehan announced that it would close all 28 of its remaining standalone payday shops in Texas. And he was candid about what he hoped to get out of the Legislature.

“Quite frankly we were hoping through the 2013 Texas legislative session to get some relief with respect to the city ordinances in Texas. That didn’t happen, and quite frankly those stores aren’t contributing any profitability to the overall equation.”

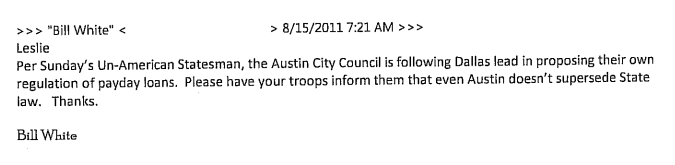

Just like his boss, William White also took an interest in the city ordinances. In an August 2011 email to Leslie Pettijohn of the Office of the Consumer Credit Commissioner, he flagged an article in what he termed the “Austin Un-American Statesman” on a proposed ordinance regulating payday loans in the city. “Please have your troops inform them that even Austin doesn’t supersede State [sic] law,” he instructed Pettijohn.

In another email he wrote that the Dallas ordinance “overreached into [Office of Consumer Credit Commissioner] territory.” As I noted in a December 2012 story, White’s position echoed almost precisely that of Cash America’s at the time.

“The industry believes the city [of Dallas] has over reached and intends to take the issue to court,” wrote Alex Vaughn, Cash America’s vice-president of governmental affairs, to Finance Commission Vice-Chair Paul Plunket. “We also believe it is under the preview [sic] of the OCCC…”

The email went on to note that Pettijohn “has taken a hard line with the respective city [sic] and informed them they had no authority to do what they planned to do and would receive no assistance from her office.” But at other times, Vaughn said, she had cooperated with the cities on enforcement and data-sharing. “Obviously we we [sic] would prefer to do everything we can to assist her with her department’s independent legal analysis of the issues involved.”

Although the backdoor pressure didn’t prevent every major city in the state, except for Fort Worth, from passing similar ordinances, White helped corral an official finance commission objection to the city ordinances. That resolution was later used by the head of the payday industry association in pressuring regulators to draft a bill blocking the cities’ local efforts to protect consumers.

As noted by Houston Chronicle columnist Lisa Falkenberg:

In April 2012, he signed the commission’s resolution complaining of the “complexity” and “confusion” of local payday regulations. He asked the Legislature “to more clearly articulate its intent for uniform laws and rules to govern credit access businesses in Texas.”

In other words, he asked lawmakers to bigfoot (or, pre-empt) local protections, forcing cities to conform to the state’s do-nothing regulation.

It didn’t happen. But it did hint at White’s true allegiances.

As the 2013 legislative session neared, the main payday industry association—the Consumer Service Alliance of Texas (CSAT)—prepared to push for legislation that would block Texas cities from establishing rules on payday and title loans. Internal emails indicate that CSAT, the Office of Consumer Credit Commissioner and representatives from major payday/title companies, including Cash America, were involved in drafting legislation.

For example, on January 23, 2013, as the legislative session was getting underway, CSAT’s point man, Rob Norcross, asked for a meeting with OCCC to discuss the legislation. Norcross wrote that he wanted to include Hurshell Brown, “our payday subject matter expert” and a Cash America executive.

“While there is general agreement on the issues addressed, some questions have arisen about the language,” Norcross wrote. “I want to make sure we get the details right.”